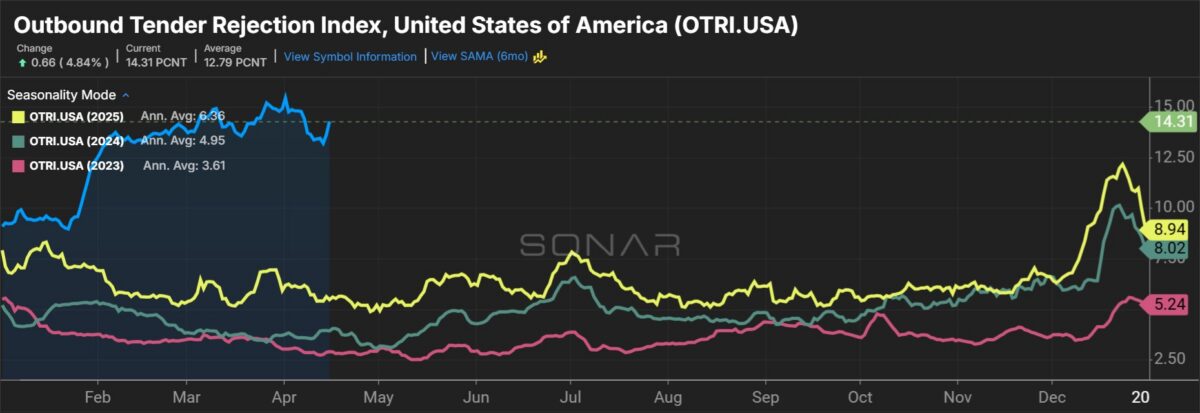

Executives at J.B. Hunt Transport Services said that there is increasing proof that tightening in the truckload market is a structural shift rather than the brief fluctuation that shippers had suggested at the beginning of the year. On a Wednesday evening call with analysts, management noted “early signs of improved demand” as “non-compliant capacity” continues to exit. It said customer conversations have become more constructive as their routing guides are failing.

J.B. Hunt (NASDAQ: JBHT) reported first-quarter earnings per share of $1.49, 4 cents ahead of the consensus estimate and 32 cents higher year over year.

Consolidated revenue of $3.06 billion was 5% higher y/y (up 4% excluding fuel surcharges), outpacing analysts’ expectations for revenue of $2.95 billion. The company said it’s taking market share across all modes. Operating income increased 16% y/y to $207 million due to cost takeouts and improved productivity.

Management updated its cost reduction program. It said another $30 million in expenses were removed during the first quarter, pushing the annual run rate to $130 million.

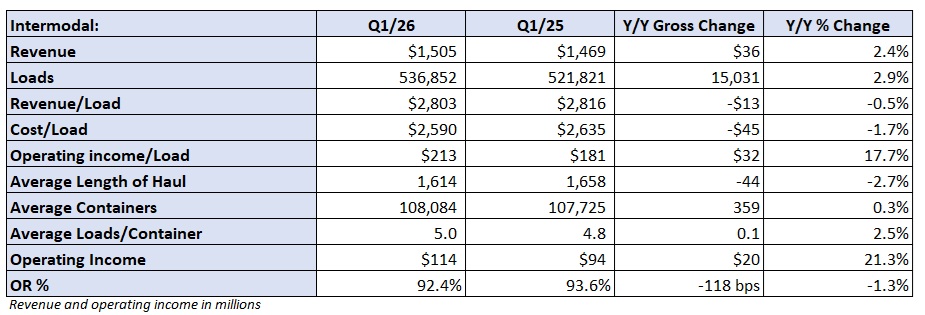

Intermodal logs record volumes; pricing hasn’t inflected yet

Intermodal revenue increased 2% y/y to $1.51 billion as load count was up 3% and revenue per load was off 1% (down 2% excluding fuel surcharges). By comparison, total intermodal carloads were flat y/y on the Class I railroads during the quarter.

J.B. Hunt reported its highest-ever volume for any first quarter, experiencing a record volume week in March (46,000 loads). By month, loads were down 1% y/y in January, up 1% in February and up 8% in March. Transcontinental volumes were flat y/y, but volumes in the East were 7% higher y/y after being up 13% in the 2025 first quarter (plus-20% on a two-year-stacked comp).

Management sounded bullish on intermodal conversion prospects, as the two primary drivers—TL rates and fuel prices—have shifted to tailwinds. Intermodal currently offers significant cost savings over TL, with FreightWaves data showing the mode is 22.5% cheaper. This is above a recent cost savings range of 10% to 15%.

J.B. Hunt didn’t provide any goalposts for intermodal pricing this bid season other than to say that price increases aren’t keeping up with inflation. Further, it said West-bound backhaul pricing was negative and that transcon pricing off the West Coast remains competitive. It is seeing better pricing in headhaul lanes and across its Eastern network.

The mix shift to the East, where lengths of haul are shorter, was a headwind to the yield metric in the quarter. (Length of haul was down 3% y/y.)

Even with only a modest revenue increase, the unit’s operating income jumped 21% y/y (operating income per load was 18% higher). A 92.4% operating ratio (7.6% operating margin) was 120 basis points better y/y. Prior cost cutting and better asset utilization (container turns improved 3%) drove the improvement.

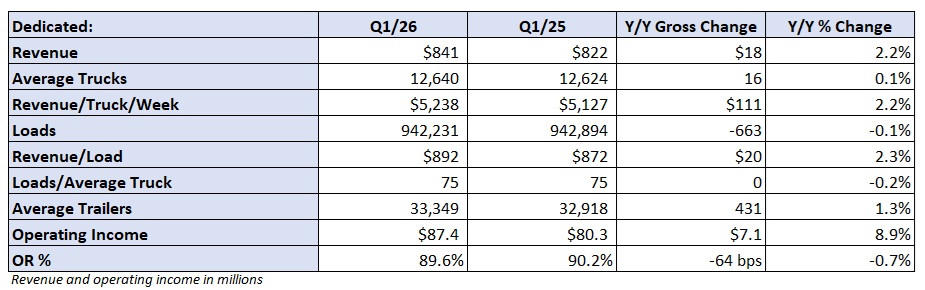

Shipper interest in dedicated solutions building

Dedicated revenue increased 2% y/y to $841 million. The increase was entirely driven by a similar increase in revenue per truck per week, as average trucks in service were flat with the prior-year quarter.

J.B. Hunt sold service on 295 trucks in the quarter and reiterated a full-year goal of 800 to 1,000 truck additions. It had its second-highest month for “new deals priced” in five years during the period, but noted that driver recruitment has become a headwind as the market has tightened.

An 89.6% OR was 60 bps better y/y even as poor weather led to incremental cost headwinds in the quarter. Also, the rough winter delayed the typical spring surge its home-and-garden customers typically experience. The company reiterated guidance for modest operating income growth this year but cautioned that new business wins are a temporary margin headwind due to the associated startup costs.

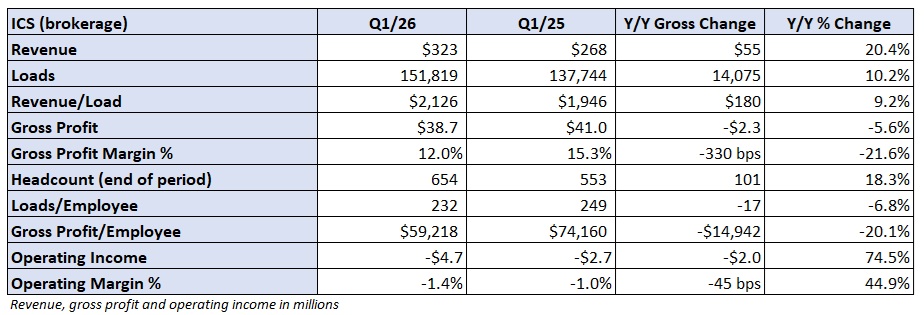

Brokerage volumes surge but losses widen

A runup in TL spot rates (purchased transportation) has compressed gross margins across the brokerage industry. J.B. Hunt’s brokerage unit reported a $4.7 million operating loss, the 13th-straight quarterly loss, and $2 million worse y/y.

Revenue increased 20% y/y, with both load counts and revenue per load contributing almost equally to the increase. A 12% gross profit margin was 330 bps worse y/y and 40 bps worse sequentially. The company is focused on repricing contracts and said it reduced direct costs, which exclude purchased transportation, by 1% in the quarter.

Other Q1 takeaways

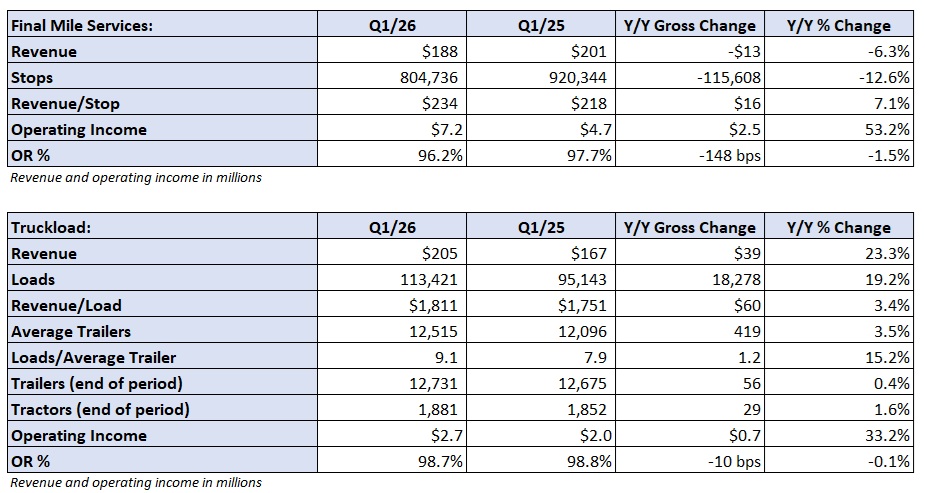

Revenue in the TL unit increased 23% y/y to $205 million as loads jumped 19% and revenue per load increased 3%. However, gross profit contracted 5% in the period as purchased transportation costs surged. Management noted that capacity is leaving the market, even with the jump in spot rates, and that drivers are becoming increasingly difficult to find. Across the enterprise, J.B. Hunt’s current need for drivers is the highest it has been since June 2022.

It said the volume surged in brokerage and TL reflect the “first part of an upcycle.”

The company previously flagged a $90-million revenue headwind this year (on $824 million in annual revenue) from the loss of a final-mile customer. However, revenue in the unit was down just 6% y/y to $188 million in the quarter. It said demand in key final-mile segments like furniture and appliances has steadied.

Shares of JBHT were up 6.7% in early trading on Thursday compared to the S&P 500, which was off 0.1%.

More FreightWaves articles by Todd Maiden:

- Yield discipline, fuel price surge driving LTL rates to new highs in Q2

- Cass data shows further freight market tightening in March

- FedEx Freight sets goalposts for standalone business

The post J.B. Hunt says TL inflection ‘structural,’ not temporary appeared first on FreightWaves.